An Appetite for M&A?

What 18 Fortune 500 Executives Think About Exit Opportunities Today

Supply Change Capital invests in the future of food with an emphasis on climate and culture. After two years in operation, we’ve welcomed over a dozen startups into our portfolio. We are constantly thinking about the exit landscape and how the economy, policy, and corporate strategy impacts the path to exit for our portfolio.

As a part of a Northwestern Kellogg School of Management independent study, Alena Marovitz worked with Supply Change Capital as an MBA Fellow. The purpose of her fellowship was to gain insights into the exit environment for the food and beverage (F&B) industry. As a part of this work, she interviewed 18 F&B executives across Fortune 500 retail and consumer packaged goods (CPG) companies. Here she shares what she learned both in terms of the market environment and their appetite for M&A.

The Market Backdrop

Supply Change Capital invests in food and agtech across the supply chain. About a quarter of our capital is allocated to CPG in our portfolio construction model, while 75% is allocated to food and agtech. Our hypothesis is that exit by M&A is going to be attractive for (F&B) startups in the near future. We believe this is the case because:

The IPO market, particularly for F&B companies, is volatile. In 2022, global IPO volumes fell by a staggering 45%. F&B companies aiming to go public have been hit even harder. According to Pitchbook, F&B company IPOs globally went from 40+ in 2021 to less than 15 in 2022 (more than a 50% reduction).

M&A for F&B companies continues to be reliable. Across all sectors, ⅔ exits typically fall under M&A, according to JP Morgan. When considering acquisitions by F&B companies, Figure 1 shows that Fortune 500 F&B acquisitions have remained steady at around 50/yr (except for a slight dip in 2020 due to the pandemic). A wide variety of sub-segments are represented in acquisitions, with food, beverage, and software products taking the lead.

Figure 1: Acquisition Data from Startups Founded after 2005 and Acquired by F&B F500 (Source: Pitchbook)

Notable recent exits include Mondelēz’s acquisition of Clif Bar for $2.9B (2022), Hershey’s acquisition of Dot’s Pretzels for $1.2B (2021), and Coca-Cola’s acquisition of BODYARMOR for $5.6B (2021).

And, more than half of CPG leaders surveyed by Bain say that corporate M&A will either increase or stay the same over the next three years (Figure 2).

Figure 2: More than Half of CPG Business Leaders Say M&A Will Increase or Stay the Same (Source: Bain)

Large food corporations are looking to startups for growth. At the Consumer Analyst Group of New York (CAGNY) conference in Feb ‘23, many Chief Financial Officers highlighted the important role that acquisition continues to play in their innovation strategies. Kofi Bruce, General Mills’ CFO, mentioned that General Mills is “acquiring to enhance our growth profile,” while JM Smucker’s CFO, Tucker Marshall, said M&A “will continue to play a role in our strategy of expanding our leadership in the categories where we participate.” Food companies in particular see greater opportunities for M&A due to synergies in scaling and the ability to complement their internal innovation.

As a result, we believe that acquisition is an important exit strategy to consider.

Fortune 500 Executive Interviews and Learnings

Since Fortune 500 (F500) M&A is going to be an important path for food startups moving forward, what better way to understand F500 challenges and needs for the future than by hearing from key decision makers at these companies directly? Over the last few months, I was thrilled to speak with nearly 20 food and beverage executives across a wide variety of companies. While I won’t divulge their respective companies or names, I am excited to share my high level insights from my conversations with them below.

Insight 1: How Executives Think About Innovation

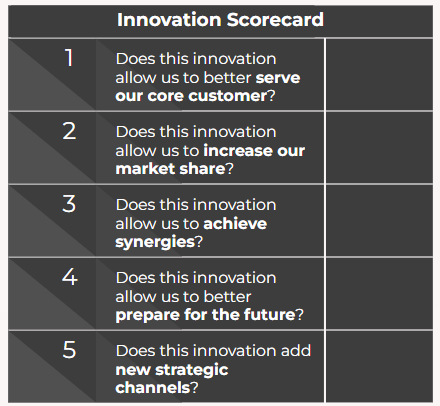

When asked about innovation through acquisition, I was intrigued to hear that the majority of food & beverage executives coalesced around five main criteria (Figure 3):

Does this innovation allow us to better serve our core customers?

Does this innovation allow us to increase our market share?

Does this innovation allow us to achieve synergies?

Does this innovation allow us to better prepare for the future?

Does this innovation add new strategic channels?

For example, one executive spoke at length about a successful acquisition that hit on most of these criteria. This person mentioned how the acquisition: a) complemented a gap in their portfolio that their core customer was gravitating towards; b) allowed them to enter a new category and gain share; c) achieved synergies by reducing input prices for the acquiree by 30% through economies of scale; and d) prepared them for the future since the acquiree’s category was growing rapidly.

Figure 3: Executive Innovation Scorecard (Source: Interviews with 18 F&B executives)

Insight 2: Startups Need to Address Real Problems

“What is the problem that you are trying to solve?”

At my last company, this point was drilled into me by my CEO over and over, particularly as I would dream up solutions without thinking about the needs of users. I heard this sentiment repeated again by my interviewees who were frustrated with startups that thought they knew the right solution without actually understanding the problems. Some great quotes from these executives include:

“You have to put the farmer first and have a farmer-centric approach rather than a brand-centric approach.”

“They get fixated on the solution and not the problem.”

For start-ups with F&B acquisition in mind, it is critical that the business being developed responds to real-world needs. This sounds simple, but it was a most repeated pain point. Some questions to consider: Have you spoken with your customers? What are their true pain points? Why are you uniquely positioned to solve this problem at this point in time? Why does solving this problem matter? In the end, taking a customer-centric approach will help startups achieve product-market fit and win over these executives.

Insight 3: Be Future Forward

There was a wide range of ideas pitched regarding what is needed in the future. Five categories ended up rising to the top as the most frequently repeated:

Traceability in Supply Chain

“Traceability” in the food supply chain has become a buzzword for over a decade. There are strong upsides to forging greater transparency in the food supply chain, including enhanced forecasting, improved freshness, more robust food safety controls, reduced food waste, reduced greenhouse gas emissions, etc. But, no player has solved this issue for Fortune 500 food and beverage companies (yet). Interviewees cited challenges with scaling traceability programs, implementing them in a host of different countries, and bringing them enterprise-wide.

Agtech that Addresses Farmer Needs

Again and again, I heard frustration from interviewees regarding agtech startups. These startups pitch executives on their solution when it is clear that they haven’t generated adoption from farmers themselves yet. This was a major turnoff for the interviewees. Dani Nierenberg’s “Food Talk” episode with Ted Matthews provides a great listen on the challenges of running a commercial farm. Many farm operators are over 60 years old and work 12 hour days. Oftentimes, farming household spouses will find second jobs since farmers don’t have insurance;only 23% of household income comes from the farm itself. Even so, many farms struggle to break even. With these in mind, it’s clear that any future agtech needs to take a farmer-centric approach to be seamless for farmers to adopt and prove the ROI.

Brands with Strong Stories

Brands with strong stories win the day. Hands down. Consider these:

The thirteen siblings trying to save their dad from cancer by selling his refrigerated peanut butter bars. A husband and wife team that began popping popcorn in their garage to teach their kids the value of hard work. The CrossFit aficionado who couldn’t find a snack that fit his paleo diet.

Stories are up to 22x more memorable than facts alone, so it’s no wonder that brands including Perfect Bar, Angie’s Artisan Treats, and RXBAR were attractive acquisition targets. Fortune 500s are increasingly looking to startups that have strong stories that align with the F500’s mission and vision.

Smart Manufacturing / Retrofitting

This one was a real shocker for me. Did you know that the average age of warehouses in the United States today is 42 years old? While it may seem that these facilities are past their expiration dates, these warehouses and manufacturing plants are not going anywhere. Especially in today’s economy, companies are not prioritizing large CAPEX projects. As a result, F500s are in need of solutions that can plug and play with their existing, aging warehouses.

Better-For-You CPG

As one of the executives pointedly said to me, “Wellness is here. It’s not a trend, it’s a mainstay.” Data supports this perspective, as the health and wellness market is expected to reach $1.6T by 2030 (with a CAGR of 7.9% over 2022-2030). Particularly as Fortune 500s are trying to claim shelf space in the perimeter of the grocery store, expect to see growth in plant-based, functional, fermented, and fungi-based foods.

Other notable categories of future innovation mentioned by multiple interviewees include inventory management technology, refrigeration energy tracking, food waste reduction, value engineering, shelf life enhancement, and ingredient upcycling.

Conclusion

This project was an insightful window into how some of our potential advisors and partners are thinking about innovation. We will leverage the learning in three main ways:

Sourcing

These executives gave us a lot of food for thought regarding areas of innovation where they would like to see more support. While we continue to build out our portfolio, we will keep the repeated categories top of mind. Additionally, when performing due diligence, we will look to make sure that potential portfolio companies have spent enough time performing customer and stakeholder interviews. As the executives mentioned, startups need to ensure that they are solving a true problem that others resonate with, rather than something they alone think is important.

Portfolio Support

Regarding our current portfolio companies, we strive to engage with and support our founders post-investment. One way we currently do this is by committing 1% of the fund for portfolio support through our Supercharge III program. In this program, our founders work with an executive coach in a cohort where they learn about various topics, including HR basics for early stage organizations, common growing pains for early stage organizations, defining culture, and the role of leadership.

After conducting this research project, we’re exploring additional ways that we can help our portfolio companies further learn from and engage with potential acquirers. We’ve found that corporate accelerators, such as Target’s Takeoff Program, have been great opportunities for our portfolio companies (including Agua Bonita, AYO Foods, and Partake) to better understand the language of F500s. Additionally, as our portfolio companies begin to partner with strategics, we will encourage them to reframe their sales point of view from “why am I great” to “why am I great AND how can I help address your specific pressing business needs with my tailored solution.”

Private Sector Engagement

Getting time on the calendars of 18 busy executives was no small feat! After these initial conversations, we hope to continue to engage with these impressive individuals. We’re planning a webinar series for them to learn more about Supply Change Capital and potential opportunities to leverage their insights as advisors to our firm. We also will be on the lookout for additional ways to partner with F&B private sector companies, whether through co-hosting pitch competitions, sitting on conference panels with them, or looping them into our network in other ways.

| A guest post by

|