Part I: Agricultural Robotics and the Future of Mechanization

An exploration of the ag-robotics landscape

Agricultural mechanization played a critical role during the Industrial Revolution, significantly increasing farmers' capabilities and the amount of land they could manage. In modern outdoor agriculture, nearly every process relies on mechanized systems that are slowly but surely being upgraded to automated robotics solutions. Broadly defined, agri-robots are machines designed to perform various agricultural tasks automatically. By functional areas, agricultural robots include – but are not limited to – planting, weeding, spraying, pest and disease control, and harvesting systems. In this landscape map, we explored the biggest opportunity for agri-robots to improve highly labor-intensive agricultural operations further.

Ag-robotics is a fast-growing category in the ag-tech investment landscape. In this two-part series, Supply Change Capital MBA Fellow and ag-tech expert Anastasia Nor takes a deeper dive.

Takeaways

Agriculture automation will likely continue to grow, driven by the critical need to address farm labor shortages and rising input costs while transforming agriculture into a safer and more sustainable industry.

Precision operations, such as highly labor-intensive tasks like weeding, spraying, and harvesting, are central to automation. In this area, robotics help simplify tasks and facilitate more informed decisions while reducing the environmental impact.

The industry is fraught with challenges, with just a few agricultural robotics companies exiting in the past decade. For robotics startups to succeed, they must focus on building reliable, cost-effective robots that deliver unique added value beyond replacing human labor.

The Market: The rising trend for drones, harvesting, and precision robots

The Agricultural Robots Market is anticipated to surge to approximately USD 86.5 billion by 2033 from a baseline of USD 13.4 billion in 2023, exhibiting an impressive CAGR of 20.5%. North America’s market is estimated at USD $5 billion in 2023 [Figure 1].

The market is segmented into field, dairy, and indoor farming. Milking robots dominated the market in 2023 with a 48.6% share. Drones (UAVs) and driverless tractors are also growing rapidly. Harvesting robots are projected to grow at a CAGR of 23.1% from 2024 to 2030, reaching USD 1.40 billion by 2030.

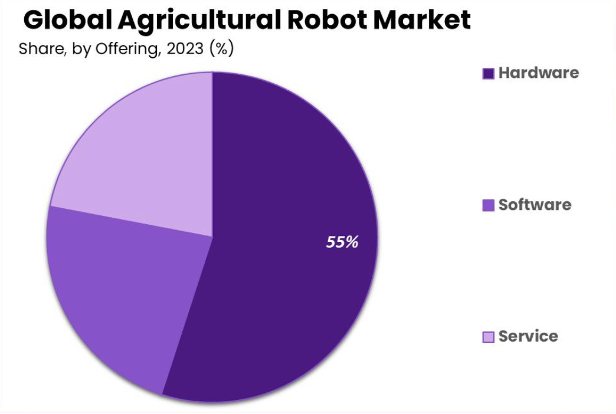

The market is divided into hardware, software, and services:

Hardware, including automated tractors, drones, and arms, accounted for over 55% of investment dollars in 2023 [Figure 2].

Software powers robot functionalities, enabling tasks like data analysis and autonomous navigation.

Services, including maintenance and support, are also crucial. In the sub-segments, planting and seeding held over 24.6% of the market share in 2023, specializing in precision planting and seeding. Soil management is expected to grow the fastest, driven by the increasing use of mobile robots for fertilizing and weeding.

Market Drivers

Labor challenges significantly impact the agricultural sector. Farmers face a high risk of injuries and have the highest rate of fatal occupational injuries in the United States. The labor shortage is one of the main factors contributing to crop waste. For example, in the United Kingdom, over 22 million pounds of fruits and vegetables were left unharvested in 2022 due to labor shortages. In the US, WWF estimates that 10 million tons of specialty crops grown on farms yearly are never harvested — equivalent to nearly one-third of what’s grown.

High input costs represent a significant concern in the agricultural sector, particularly considering recent supply chain disruptions and geopolitical issues. These challenges have increased the prices of key fertilizers — such as urea, diammonium phosphate, and potash — by over 15 percent annually over the past five years.

Regulation is driving a shift toward more sustainable agricultural practices globally. For instance, the European Green Deal aims to drastically reform European agriculture by 2030, targeting a 50 percent reduction in pesticide use from 2020 levels and transitioning 25 percent of agricultural land to organic farming to minimize synthetic inputs. In Canada, there's a push for farmers to cut fertilizer use by 30 percent from 2020 levels by 2030; those failing to meet targets may miss out on $1.1 billion in government aid for greener farming equipment.

Consumer interest in a more sustainable food system is rising, pressuring farmers to adapt their production methods downstream. In response, consumer-packaged goods (CPG) companies are making significant environmental commitments concerning the sourcing and cultivation of their raw materials. For instance, Nestlé has committed to achieving net-zero emissions by 2050, enhancing the traceability of its raw materials, and reducing chemical use on farms by 2030.

Challenges: High cost and unclear ROI are the biggest farmer barriers to adoption

According to McKinsey's 2022 survey involving 5,500 row and specialty crop farmers across Asia, Europe, North America, and South America, AgTech adoption shows significant geographical variation.

High upfront cost was cited by 52 percent of North American farmers as the major barrier to adopting farm management systems [Figure 3]. For example, fruit-picking robots, which need further development in sensing, manipulation, and soft robotics, are prohibitively expensive — costing between USD 250,000 and USD 750,000 — making them unaffordable for most farmers. To address this, many companies are considering leasing options to improve accessibility. Although drones are currently used, industry experts predict that fully autonomous agricultural robots, like driverless tractors or weeding robots, will not be widespread until post-2025.

Uncertain returns on investment (ROI): Farmers often hesitate to invest in AgTech due to uncertainty about the economic benefits and ROI, especially in the short term. The potential long-term gains may not justify the immediate high costs for some. 40% of North American farmers pointed to unclear ROI as their biggest challenge in adopting farm management systems. Offering AgTech solutions through a subscription or pay-per-use model, reducing the need for large upfront investments, could be a potential solution to address this problem.

Complexity in setup and use is a major barrier to AgTech, especially for farmers with limited technical expertise. Many AgTech tools, such as precision agriculture hardware, sensors, drones, and farm management software, require intricate installation processes and specialized knowledge to operate effectively. In Europe, 32% of farmers reported this issue as a critical challenge, while the high cost remained at the top of the minds of 48%.

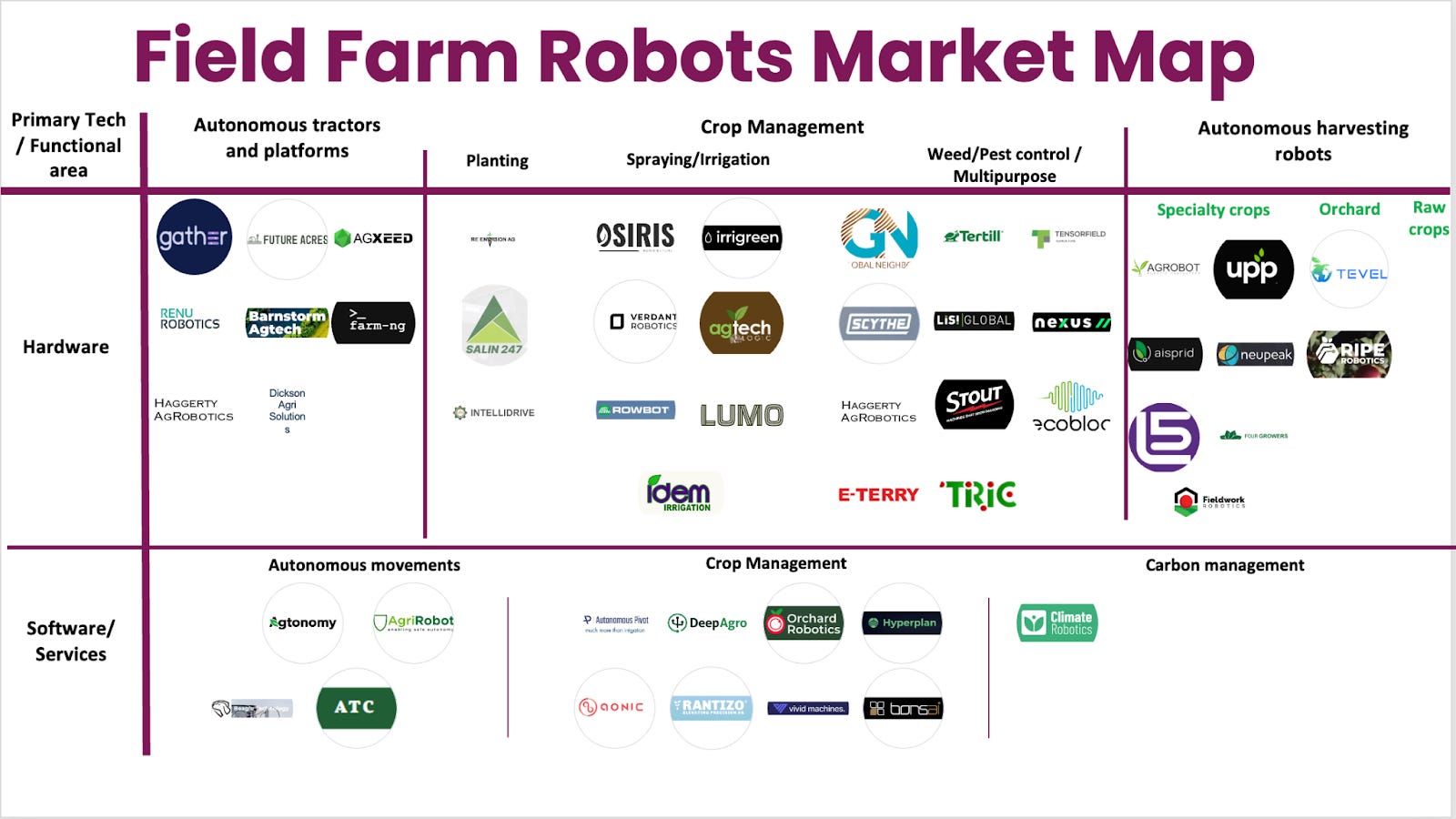

Field Farming Robots Market Map

Due to the opportunities and challenges, a robust field of innovations is coming to market. The field farming robots’ landscape [Figure 4] is segmented vertically by functional areas:

Autonomous tractors and platforms

Crop management (Preparing and Planting/Seeding)

Spraying and spreading; Weeding, Thinning, and Pest Control)

Harvesting (autonomous, semi-autonomous harvest robots).

The landscape is also segmented vertically by the primary product technology, which includes hardware, software, and services. This landscape map focuses on early-stage start-ups, from pre-seed to Series A.

Agricultural UAVs and automated harvesting machines held the largest Agriculture Robotics market share in the field farming category in 2023, while investment in precision systems is on the rise.

Aerial Imagery Drones and Seed-Planting Drones (UAVs): UAVs represented the biggest market share of agricultural robots in the field farming category. UAVs or drones are revolutionizing agricultural robotics by enabling a wide range of precision farming applications. They can capture high-resolution multispectral and hyperspectral imagery to monitor crop health, detect nutrient deficiencies, and detect diseases early, to name just a few use cases.

Notable companies that have shown great results in agricultural imaging, seed planting, and cloud seeding include American Robotics, Pixxel, and Aerospacelab.

Agricultural Robots in Crop Harvesting: There has been a significant investment in harvesting robots capable of performing various agricultural tasks with minimal human intervention. These technologies aim to address labor shortages and increase efficiency in the field. Crop Harvesting Robots are divided by functionality into Autonomous, Semi-autonomous, and Specific Task-Focused Harvesting Robots. Agricultural robotics startups focused on harvesting solutions are primarily targeting high-value, labor-intensive crops: soft fruits and berries (e.g., strawberries, raspberries, and blueberries), tomatoes, orchard fruits, and some specialty crops (e.g., broccoli, artichokes).

A few notable companies in the space include Harvest CROO Robotics, Tortuga AgTech, Fieldwork Robotics, Tevel, and Ripe Robotics.

A note on specialty crops

While row crops like wheat and soybeans are quickly harvested with combines, specialty crops like strawberries remain widely hand-picked. So, why haven’t more specialty crop growers embraced mechanization, and should we expect a greater focus of agrobotics startups on specialty crops?

Specialty crops pose significant challenges for agricultural robotics due to the delicate handling required during harvesting to avoid bruising or damaging delicate fruits and vegetables. These crops are grown in highly unstructured environments like orchards and vineyards with varying terrain, complicating autonomous navigation and robot operation. Additionally, specialty crops exhibit high variability in physical characteristics even within the same species, making it difficult for robots to identify and handle the crops accurately.

Despite these challenges, specialty crops are more attractive for agricultural robotics startups because they have higher value and profit margins than row crops. This provides a greater incentive to develop robotic solutions that can reduce labor costs, increase efficiency, and maximize margins for these high-value crops.

In summary, specialty crops' greater complexity and higher value make them a more attractive frontier on which agricultural robotics startups can focus their innovation efforts.

Agricultural Robots in Weeding and Mowing: Startups that develop robots for precision weeding and pest control have attracted VC funding. These robots can significantly reduce the need for chemical herbicides and pesticides, thus reducing farmers’ costs while promoting more sustainable farming practices.

Some notable startups in this area include Carbon Robotics, FarmWise, Naio Technologies, and Blue River Technology. They have developed robots for weeding and targeted spraying, reducing herbicide use. Naio Technologies, for instance, has developed three distinct robots designed to assist farmers in various tasks, including hoeing fields, weeding vegetable crops, and maintaining vineyards. One notable example of their innovative solutions is the company's partnership with the renowned Château Mouton-Rothschild, where they deployed their vine-tailored robotic weed killer, Ted, in the prestigious vineyards.

Investing in AgTech: Upward trend for Farm Robotics despite the overall decline

The AgTech sector experienced a decline in VC deal value and count in Q4, totaling $1.4 billion across 181 deals, according to Pitchbook’s Q4 AgTech Report. The quarterly deal activity declines in 2023 have added up to nearly a 40% reduction in deal values and deal counts in 2023 – $7.1 billion invested across 952 deals, down 39.5% and 39.2%, respectively [Figure 5].

Despite the decline, funding to upstream startups operating on the farm or in food production accounted for 62% of overall dollar investment in 2023, up from 51% in 2022 to 30% in 2021. Top VC investors in AgTech companies since 2023 are shown in Figure 6.

Farm Robotics, Mechanization, and Equipment category grew in 2023, showing a steady upward trajectory for some time now and increasing 9% year-over-year to $769 million [Figure 7]. Asia led the investment in the category, largely thanks to Indonesia’s eFishery, which raised a mega $200 million Series D in 2023, taking it to unicorn status. The Americas, which garnered the most investment dollars in 2022, saw less funding but slightly more deals than Asia.

Many lessons can be learned from the ag robotics startups that have successfully scaled. We explore this and more in Part II: An Analysis of Success Factors for Ag Robotics Start-Ups.

|