Technologies enabling long-term health outcomes for GLP-1 users

Making lasting health and lifestyle changes seamless, during and after treatment

Summary

GLP-1 prescription drugs have dramatically transformed the diet and nutrition landscape in the United States. 12% of adults had used a GLP-1 prescription drug as of May 2024, and global spending is expected to multiply from $6 billion in 2023 to $105 billion by 2030.

The cataclysmic shift in food consumption for GLP-1 users shows early signs of positive health outcomes: GLP-1s have proven effective in managing blood glucose control and weight and improving the symptoms of diet-related disease like Type 2 diabetes and heart disease. More than 50% of American adults have a diet-related disease, such as heart disease, type 2 diabetes, obesity or some forms of cancer. These early results provide a promising solution to a large segment of the US population struggling with the symptoms of diet-related disease.

Holistic support services will be critical to successful long-term outcomes. Despite the proven effectiveness of GLP-1s, adherence remains a major challenge, with only 32% of patients continuing treatment after one year. When consumers stop a GLP-1 drug, the health benefits experienced are often eroded: a preliminary study showed that those who stopped taking GLP-1 prescriptions on average gained two thirds of lost weight back, diminishing the health benefits of the drugs over time.

This analysis will dig into the food and health technologies that support GLP-1s users during and after prescription, emphasizing areas of opportunity for venture investment. In our analysis, we will focus on the particularly strong opportunity for tech-enabled companion products that help GLP-1 patients make food and lifestyle choices with ease.

The Market

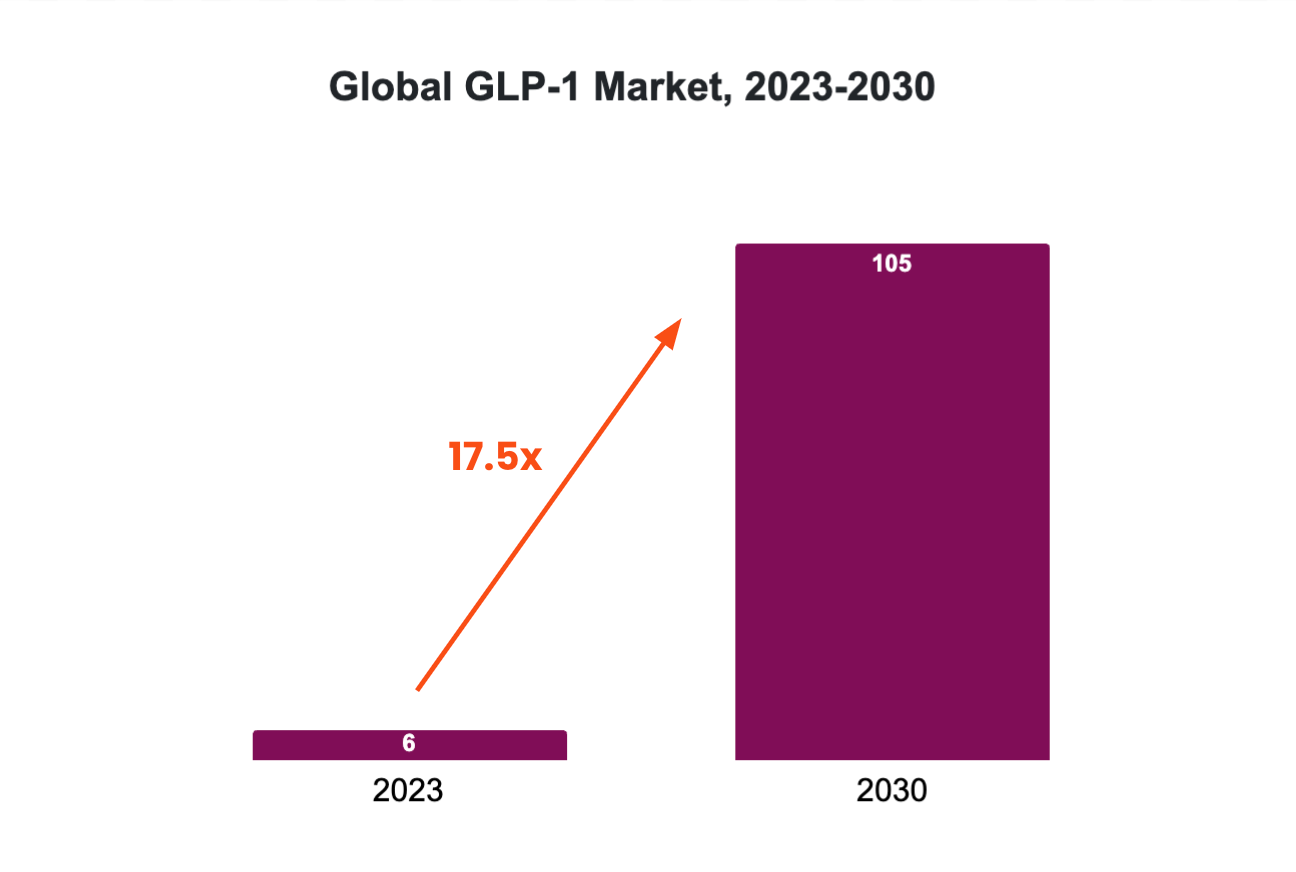

The global GLP-1 market is exploding

In 2023, global spending on GLP-1s represented $6 billion in value. In the next 5 years, the market is expected to grow to $105 billion, representing a 17.5x increase in market value:

By 2030, the US GLP-1 patient pool will include 15 million people, representing 9% of Americans with diet-related diseases. This massive increase in adoption has implications for a range of industries, from pharmaceuticals to food and health technology.

What are GLP-1s?

GLP-1s mimic a natural hormone in your body that helps control blood sugar and makes you feel full after eating. They work by slowing down how quickly food leaves your stomach, which helps you feel satisfied longer, and by signaling to your brain that you're full, reducing hunger and food cravings.

Since GLP-1 prescription drugs were approved for use to address health conditions outside of diabetes in 2021, several drugs have become available to Americans looking to improve their health and lose weight. Among the most prominent are:

Semaglutides, known as Ozempic/Wegovy (Novonordisk)

Tirzepatides, known as Mounjano/Zepbound (Eli Lilly), and

Liraglutides, known as Victoza/Saxenda (Novonordisk).

Eli Lilly, the producer of Mounjaro/Zepound GLP-1 injections, recently announced promising results from clinical trials on a new form factor – a GLP-1 pill that is taken orally. New form factors have the potential to increase GLP-1 use and retention, especially in cases where the cost and complexity of delivering the prescription is reduced.

Solutions & Gaps

Existing solutions are built on top of established business models including DTC prescriptions, meal delivery kits, and telehealth

Late-stage/public companies in telehealth and meal delivery capitalized on GLP-1 offerings with a range of supplemental products or offerings for GLP-1 users.

Across existing and new providers, there are 50+ companies that patients can work with to secure a GLP-1 prescription with varying levels of coaching and support. There are several tech-enabled methods for securing GLP-1 prescriptions that have taken off:

Existing Telehealth Providers. Many telehealth providers of nutrition support or general telehealth services are now offering GLP-1 prescriptions and support, including platforms with millions of users like Noom (Series F) and WeightWatchers Clinic (public).

Existing DTC Prescribers. Direct-to-consumer prescription companies like Hims & Hers (public) and Ro (Series E) have expanded their offerings to include GLP-1s amidst rising popularity of the drugs.

Fast-Growing GLP-1 Telehealth Providers. There is also a growing segment of new entrants to the GLP-1 telehealth market, with companies like Found and Mochi Health accelerating growth in the years after GLP-1 approval.

As the range of options expands but prices vary from provider to provider, companies like GLP Winner are also emerging to help patients find the right provider for their needs.

Outside of telehealth, a range of existing solutions have pivoted and seen success in the rise of GLP-1 use. Meal delivery services like Factor (acquired) and Daily Harvest (Series D) adjusted meal plans to offer GLP-1 friendly programs.

We captured the full range of companies in the GLP-1 support services market in our analysis:

The gap and opportunity: hyper-personalized solutions

Though established players in telehealth and meal delivery were quick to pivot and offer prescriptions and meals for GLP-1 users, there remains a gap in personalized, incredibly easy to use companion products that help GLP-1 users make decisions in their day-to-day lives. When at the grocery store, how do you make sure you’re choosing the right products without doing endless research or reading the ingredient label and nutrition panel for each and every product? When you go out to dinner, what exact dish should you choose on the mom-and-pop restaurant’s menu? What activity or exercise should you be getting in the morning before you drop your kids off at school, and how do you make the time for it?

Companies like Nourish and Allara Health provide coaching to help GLP-1 users and other patients with these shifts in lifestyle and food choices on a 1:1 basis. They’ve seen success with GLP-1 users: Nourish, for example, demonstrated improved adherence and maintained weight loss for their GLP-1 patients.

However, though these subscriptions are often covered by payers, increasing access, there is a fundamental issue with scale and frequency. By relying on 1:1 interactions, there is a limit on how many patients can see a specialist, such as a nutritionist, on a frequent basis.

This issue of scale creates an opening for AI-based companion products that provide supplemental support based on a specialist’s advice. For example, we’d love to see solutions that accompany GLP-1 users while they’re shopping for groceries, in-person or online, recommending meals and product purchases that align with the personalized diet recommended by their nutrition coach. Similarly, coaching tools that provide personalized, daily recommendations on food choices and lifestyle to augment the support of 1:1 coaching present a scalable, impactful opportunity.

There are three key areas for investment in support of GLP-1 adherence and long-term success:

1. Tracking, Coaching & Companions

Companion products have the potential to help GLP-1 patients stay on their prescriptions by removing the complexity of taking the drugs. Medication tracking app Shotsy, which helps users keep track of their injections, reached 100,000 downloads in just 8 months. Other companion products make it effortless to choose foods aligned with the dietary goals of GLP patients, providing personalized recommendations based on factors like cultural preferences, lifestyle, and other dietary restrictions or preferences (such a gluten intolerance or vegetarianism). Solutions include:

Digital companions with personalized, gamified approaches

Personalized grocery shopping integrations that require minimal manual input

Personalized, tech-enabled nutrition coaching that make healthy eating effortless while respecting food preferences

Medication tracking apps

Ex: Shotsy, Sidekick Health, Verve Market, bitewell

2. Telehealth

There are a range of telehealth solutions that help GLP patients get prescriptions, receive nutrition/fitness coaching, and connect with healthcare providers in support of their goals while on the prescription. Some solutions like Allara Health also support patients after they end the prescription with continued nutrition coaching and support for other health conditions they may have. With the wide array of telehealth solutions available, there are also emerging solutions that connect patients with the right provider and program, like GLP Winner. Solutions include:

Personalized virtual care for GLP-1 users

Personalized, evidence-based curricula for developing sustainable health habits

Products helping GLP-1 users find the right telehealth solution for their budget and needs

Ex: Calibrate, Found, Allara Health, GLP Winner

3. Meals, Food & Supplements

Food products, meal delivery services, and supplements that are specifically tailored to GLP-1 patients can help during and after GLP-1 use. Patients may start using a product or service while they are on the prescription, and then maintain use after they’ve stopped, ideally slowing or preventing the weight gain that has been associated with the end of a GLP-1 prescription. Solutions include:

Personalized meal kits designed for GLP-1 users

Personalized supplements to boost GLP-1 production naturally

Pre-biotic food products and ingredients

Ex: Supergut, Trifecta Nutrition

Venture Ecosystem

The landscape for venture-backed startups providing technology solutions to GLP-1 users is emerging, but several tech companies that pivoted to offer GLP-1 prescriptions and services have exited or raised significant growth rounds in the last five years:

Hims & Hers (publically listed, 2021 SPAC). The company went public with a valuation of $1.91B in 2021, and has since grown to an enterprise value of $5.96B (as of April 25, 2025).

Investors included top consumer VCs Redpoint and Forerunner

Omada Health (Series E) and Virta Health (Series E). Both telehealth companies are seeing 4x user growth and 60% revenue growth, fueling speculation for potential IPOs. To date, Omada has raised $450M, while Virta Health has raised $365M.

Omada investors include a16z and healthtech VCs like Kaiser Permanente Ventures and Rock Health Capital.

Virta investors include Sequoia Capital and Tiger Global as well as healthtech VCs like Obvious Ventures and Rock Health Capital.

The growth of GLP-1 use has also led to early acquisitions: in 2023, Weight Watchers acquired Sequence, a Series A telehealth company that prescribes GLP-1 drugs and provides support comprehensive services, for $132M. This is likely the first of several acquisitions in the space, as companies focused on behavioral and nutrition support look to add the capacity to prescribe and support GLP-1 use. Players including Eli Lilly have taken a partnership strategy to date, working with DTC prescription companies like Ro and telehealth providers including Teladoc. Lilly is well positioned to acquire and grow a telehealth platform through internal investment in Lilly Direct, which is focused on enabling DTC access to all Eli Lilly GLP-1 pharmaceutical products.

Where we’re investing our time and capital

Supply Change Capital’s broader health thesis around personalized solutions that make it easy for people to eat according to their nutrition and dietary needs aligns well with the opportunities arising in GLP-1 companion products.

Last year, we made two investments in the space:

Verve Market – a hyperpersonalized online grocery platform that helps consumers discover, plan and shop according to their dietary restrictions or preferences, effortlessly.

bitewell – a nutrition intelligence tool that partners with grocery retailers such as Kroger to help customers intuitively and quickly understand the nutritional value of foods in their carts.

Though these companies are not targeting GLP-users exclusively, each provides personalized, easy-to-use support for anyone who wants to maintain a healthy lifestyle or make a change in the way they eat. Both act as excellent companion technologies for GLP-1 users as they transition to eating different foods and products from CPG brands than they have historically, while still providing the choice and flexibility that users want.

Conclusion

Innovative business models that improve GLP-1 adherence have the potential to grow into the next generation of diet and nutrition giants, enhancing health and nutrition outcomes for millions of Americans. We believe the most promising opportunities lie in solutions that are personalized, easy to use, and integrate seamlessly into patients' lives both during and after GLP-1 treatment.

We're actively seeking early-stage founders innovating in GLP-1 treatment support with a focus on the following solutions:

Tracking, Coaching & Companions: Personalized nutrition platforms that make healthy eating seamless and digital companions that integrate with the grocery shopping experience;

Telehealth: Low-friction, specialized telehealth services

Meals, Food, & Supplements: Differentiated GLP-1 consumer products that are delicious and deliver results for a massive audience

If you’re building in the GLP-1 space, we’d love to hear from you! You can share your opportunity here.

As a next step in our research on GLP-1s, we’ll take a deep dive into the food industry to understand how food companies, large and small, are approaching GLP-1s and the broader consumer health trends associated with them. Stay tuned!

| A guest post by

|