The Rise of Novel Cocoa Alternatives

As the traditional cocoa market is driven to an inflection point, novel cocoa alternatives are positioned to disrupt the chocolate industry

The global cocoa market is experiencing unprecedented strain as prices reach historic highs, shrouding uncertainty over the future of chocolate as we know it. The problem is multifold and could create the perfect storm to give rise to novel cocoa alternatives.

Cocoa prices have skyrocketed, surpassing $12,000 per metric ton in April, an over 90% surge since the start of the year. To insulate customers from price swings, shrinkflation has begun to spread through the market as chocolate manufacturers use less cocoa or reduce product sizes. All the while, demand for chocolate has remained resilient. Global chocolate confectionery revenue is expected to reach $133 billion this year and $168 billion by 2029.

Côte d’Ivoire and Ghana have long been the backbone of the world’s cocoa production, supplying nearly 60% of all cocoa. However, pesticide-resistant crop diseases, climate change-induced droughts, and extreme weather events are ravaging their crop supplies, contributing to an almost 11% decline in global cocoa supply for the 2023-2024 season. The lack of resilience reflects an underinvestment in cocoa farms and farmers. Of the nearly 60 million farmers working directly in the cocoa sector, nearly 90% are smallholder farmers who remain in poverty despite industry efforts to the contrary. As they reach a financial tipping point, farmers are exiting cocoa production in search of more profitable crops or migrating to neighboring countries in search of more fertile land.

Regulators are beginning to recognize the social and environmental challenges of the cocoa crop. The 2023 European Union deforestation regulation requires commodities like cocoa, coffee, and cattle to be guaranteed deforestation-free, tackling growing concerns that protected land is being converted from forest to agricultural use.

The cocoa market is at an inflection point, and the industry is looking for alternatives. Novel cocoa production approaches are one angle the industry is exploring—and investing in—to keep up with global chocolate demand. Food alternative technologies have demonstrated the potential to reshape the competitive landscape for commodities like meat and dairy, and there is a similar opportunity to relieve pressure on the strained cocoa supply chain.

The role of alternatives

Current cocoa alternatives include cell-based cocoa and fermentation-based cocoa. Each solution offers the potential to address the price volatility, supply constraints, and environmental and human rights concerns associated with traditional cocoa cultivation.

Cell-based cocoa presents a sustainable avenue to recreate cocoa's exact taste and texture. It is produced by isolating cells from a cocoa bean and culturing them in a nutrient-rich liquid medium to multiply and produce cocoa butter inter-cellularly. The cocoa butter is then extracted, purified from the harvested cells, and formulated for taste. Fermentation-based cocoa solutions eliminate cocoa entirely from the production process and instead ferment inputs like seeds or oats to emulate cocoa’s flavor.

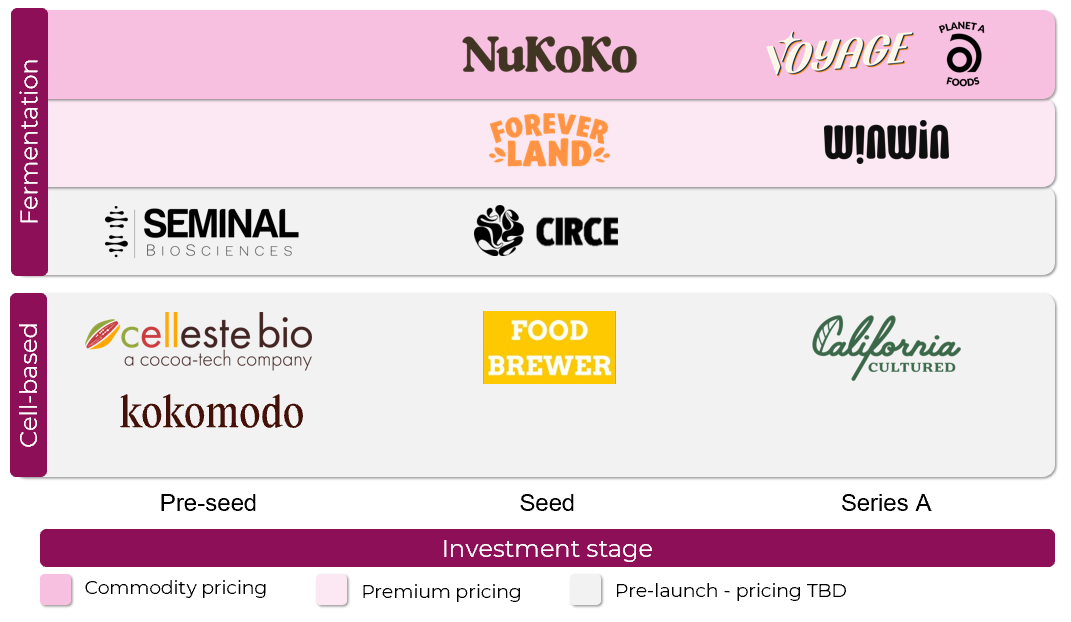

Cocoa alternatives landscape map

Several commodity and premium fermentation-based solutions are on the market, and competition is increasing among early-stage cocoa alternatives. In addition to our traditional investment analysis, we apply the price, taste & texture, and convenience (PTC) framework to evaluate the potential of cocoa alternatives and identify those that may be positioned for long-term success.

While demand for premium and specialty chocolates continues to rise, the taste and texture of a hand-crafted chocolate bar are challenging to replicate and pose an uphill battle to gain widespread consumer acceptance. We are focused on cocoa technologies that can provide a mass-market solution to the cocoa crisis in order to achieve the required economies of scale and impact.

These include solutions that (1) constitute a one-for-one replacement for tree-grown cocoa and can be used to create a full chocolate bar, and (2) can be applied in smaller-format finished goods (e.g., chocolate chips, syrups) for bakery or dairy applications. In the latter case, chocolate constitutes only a small part of the overall taste and sensory experience. This dual approach allows alternatives to integrate smoothly into existing markets while reducing consumer focus on the novelty of the product and how it might vary from traditional cocoa, potentially accelerating consumer adoption.

Key questions to consider when evaluating novel cocoa alternatives

Price parity - cocoa alternative is the same price or lower than tree-grown cocoa

Does the product have a path to parity with tree-grown cocoa prices today - $12,000 per metric ton?

Does the product have a path to parity with forecasted tree-grown prices over the medium-term - $6,000 per metric ton?

Can the product ever reach the previous price of $2,500 per metric ton?

Is there a techno-economic analysis (TEA) in place that models the timeline to price parity?

Taste & texture parity - cocoa alternative offers the same, indistinguishable taste and texture as tree-grown cocoa

Has customer feedback validated that the product achieves taste and texture parity with tree-grown cocoa?

Have B2B players validated that the cocoa alternative has the same functionality as conventional cocoa?

Convenience - the final product is as accessible to consumers as tree-grown cocoa products

What go-to-market strategy has been established to ensure the products will be as accessible as conventional commodity chocolates?

What partnerships have been formed, or could be formed, to enable mass-market accessibility?

Price parity

Cocoa alternatives must achieve price parity with tree-grown cocoa to achieve mass-market adoption by B2B players. In this commoditized market segment characterized by thin margins, willingness to pay a premium for an ingredient that competes with conventional cocoa could limit uptake.

Prior to the price spikes in 2024, the previous all-time high in nearby Intercontinental Exchange cocoa futures was in July 1977 at $5,379 per metric ton. While cocoa prices spiked to over $12,000 per metric ton in Q2 2024, analysts forecast that prices could come down slightly in the medium term to ~$6,000 per metric ton. This volatility is driving demand for cocoa alternatives and creating a runway for them to operate at higher prices while maintaining price parity in the near term as tree-grown cocoa prices settle into a ‘new normal.’

Price parity has often been a point of concern across alternative food categories. Cell-based cocoa has a potentially accelerated path to price parity versus other lab-grown products like cultivated meat. Plant-based cells are simpler to grow and require less complex media compared to animal-based cells. Cell-based meat also requires a more intricate structure than cocoa. While this suggests that scaling up cell-based cocoa might be less costly than cell-based meat, it will be essential for these solutions to have a clear path to price parity as they enter the market.

Precision fermentation has been viewed as a less expensive production pathway than other emerging cocoa alternatives technologies like cell-based cocoa. It could enable players to more quickly achieve price parity in the near-term. For example, Planet A’s fermentation-based cocoa products are reportedly 20% less expensive than tree-grown cocoa products.

Taste & texture parity

The concept of cocoa alternatives is not new. Carob has a long history of being positioned as a healthier, more environmentally sustainable cocoa alternative, but it struggled to gain widespread adoption due to its distinct, sweeter, nuttier flavor profile and texture.

As taste is the primary driver behind chocolate purchasing decisions, offering a taste and texture experience that is parallel to tree-grown chocolate is imperative to achieving widespread consumer acceptance. Novel production pathways have unlocked new potential to improve the taste, texture, and functionality of alternatives to more closely emulate cocoa. Replicating the rich and complex taste of traditional chocolate has proven challenging for fermentation-derived chocolate. More broadly, consumer ratings highlight that certain varieties of plant-based chocolates still fall short on taste, indicating a need for continued investment to refine performance.

Cell-based cocoa player California Cultured describes their technology as allowing them to produce cocoa with identical characteristics to any chocolate bar you will find in the store, down to the last molecule. Given the potential to replicate the exact sensory experience of traditional cocoa, cell-based alternatives may be able to achieve parity on this dimension sooner, accessing a critical gateway for rapid consumer uptake.

Convenience and the role of partnerships

“Convenience” is the extent to which the product is readily accessible to consumers. Securing strategic partnerships early in the novel ingredients industry - perhaps earlier than other venture-backed verticals - can be a critical enabler to achieving scale and becoming widely available to consumers.

The commodity chocolate market is dominated by a few household names like Hershey's, Mars, Godiva, Dove, and Lindt. Existing distribution agreements, economies of scale, and a pattern of consolidation across the industry have made it challenging for independent candy makers to achieve mainstream success. While incumbents can afford to pay massive slotting fees to secure shelf space and keep up with growing demands for discounts amongst retailers, newer entrants may struggle to make these financial concessions, delaying their timeline to scale. Attempting to compete with these industry giants and achieve the same level of brand recognition presents a challenge for new players trying to break through the noise and novelty of their innovations.

Forming early strategic partnerships with incumbents could be a critical step toward accelerating commercial-scale production and expanding into retail shelves. Such partnerships can also allow new entrants to access a global customer base and integrate into established product formats that have already garnered deep customer loyalty.

The role of functional & nutritional benefits

While not an essential determinant of success, offering enhanced nutritional profiles could be a notable differentiator between alternatives and presents a compelling market opportunity.

As chocolate sales reach all-time highs, consumer expectations for their chocolate continue to evolve. The National Confectioners Association found that 44% of adults are interested in trying chocolate or candy that is either sugar-free or low in sugar, up from 31% in 2020. Not only is this driven by a growing desire to reduce sugar intake, but 36% of Gen Zers cited preferring the taste of low-sugar or sugar-free items.

Chocolate incumbents have already begun expanding their portfolios to include more functionally and nutritionally diverse options, as seen with Lindt expanding its dairy-free portfolio with the launch of vegan Lindor truffles. Nutraceutical firms are increasingly leveraging confections to deliver dietary supplements, incorporating health-supporting ingredients like elderberry and black currant into indulgences like gummies or chocolates. Partnerships evidencing this trend include HP Ingredients' and Immunity Goodness launching chocolates containing tongkat ali. There is an opportunity for cocoa alternative brands offering enhanced nutrient profiles to tap into the rising demand for healthy confections to form strategic partnerships to accelerate their path to scale.

Who will win?

Several fermentation-based alternatives have already hit the market and demonstrated exciting traction against the PTC framework. In terms of price, players like Planet A Foods, Voyage Foods, and Nukoko, appear to be targeting mass-market applications, indicating an effort to compete on price with tree-grown cocoa. In terms of convenience, several players have recognized the advantage of partnering with large incumbents and secured impressive partnerships. Voyage Foods has a commercial partnership with Cargill, Planet A Foods has launched a vegan chocolate bar with Lindt and private-label products for German retailer REWE, and WNWN Food Labs is partnering with pastry and dessert producer Martin Braun-Gruppe. However, concerns over fermentation-based solutions’ ability to exactly replicate the taste and texture of tree-grown cocoa could hinder their ability to win in the long term.

While fewer cell-based alternatives have reached commercial scale, the technology is nascent. The promise of replicating the taste and texture of traditional chocolate has the potential to rapidly disrupt both the mass and premium cocoa markets and warrants close monitoring. Players like Kokomodo have claimed that they can ensure controlled, consistent-quality cocoa that offers the genuine aroma, flavors, and sweetness of tree-grown cocoa. Ultimately, it will be critical to observe how these players are able to move down the cost curve toward price parity and secure the necessary partnerships to ensure their products are conveniently accessible.

Which market is next?

The challenges faced by cocoa are significant but no longer unique. Notably, the coffee market may be on a similar trajectory, indicating a unique opportunity for novel alternatives. Despite accelerating coffee demand, prices have reached a 29-year high due to geopolitically and climate-induced supply shortages. As seen with cocoa, a growing presence of cell-based, fermentation-based, and other novel beanless coffee brands have entered the market to alleviate supply pressure and present novel, sustainable, and often healthier alternatives to traditional coffee. This includes fermentation-based player Minus Coffee, a Supply Change Capital portfolio company.

The future of cocoa

We believe cocoa alternatives have a place in the market alongside farmer-produced, tree-grown cocoa. As the global cocoa market generated nearly $13 billion in revenue in 2023 and is expected to grow to $17 billion by 2028, there is room for many solutions and technologies to capitalize on and enable this growth. We believe that both tree-grown and fermentation-based or cell-based solutions can exist harmoniously on the market — and even complement one another. This may entail targeting different segments of the market or even blending beanless and tree-grown cocoa together into a single, cohesive product with enhanced flavor. This approach is already being taken in the coffee alternatives market with products like Atomo X Bluestone Lane Remix, a mix of 50% Atomo beanless coffee and 50% Bluestone Lane’s Flagstaff coffee blend.

Countless commodity markets are grappling with yield downturns from climate change, market and regulatory scrutiny, and the resulting price pressures that threaten already thin margins. The path of the cocoa market can offer valuable insights into the potential role of innovations like alternatives as we strive for a more stable, sustainable, and equitable global food system.