Exploring Food Ecosystems Through A Heritage-Inspired Lens: Latinx Edition

At Supply Change Capital, we believe that culture is a key driver of food ecosystems. From dietary preferences and consumption patterns to agricultural practices and economic mobility, culture has played a major role in the evolution of global food systems. It continues to be a driving force behind innovations such as flavors, ingredients, and products in the US. With this in mind, our team was inspired to do a deep dive into various food ecosystems through a heritage-inspired lens to better understand (i) the emerging trends across cultures, (ii) historical investment data, and (iii) the opportunity space for both entrepreneurs and investors.

Latinos make up 19% of the US population, making them the largest racial or ethnic minority in the country (US Census). They represent a $3.2T U.S Latino Gross Domestic Product (GDP), which is equivalent to the 5th largest global economy (LDC Report). Furthermore, Latino businesses contribute $800B annually to the US economy (LBAN Report). In this inaugural edition, we explored Latinx-inspired food brands.

Key Takeaways & Opportunities

Amongst Latinx-inspired brands, companies founded by men and women mirror the population distribution of the United States (50% are female-led, and 50% are male-led). Among the Latinx-inspired brands evaluated for this study, women-founded brands have received 62% of investment capital.

Mexico’s influence on American cuisine is continuing to grow as it becomes increasingly popular amongst Hispanic and non-Hispanic populations.

According to our analysis, there is a strong concentration of Latinx-inspired brands in American states like California (21), Texas (10), Florida (8), and New York (7), which closely mirrors the distribution of the Latinx population across the United States (US HHS Office of Minority Health).

Beverages are the dominant product category, representing ~40% of the startups we evaluated for this report.

Though 25.7% of the US Latinx population identifies with Caribbean or Central American heritage, less than 10% of all Latinx-inspired companies represent Caribbean and Central American flavors and cuisine, signaling an opportunity for products representing these regions.

We see an opportunity for “better-for-you” desserts, given that various dessert categories like confectionery products and frozen desserts have a market size of ~$80B (Grandview Research, Grandview Research) and growing. Additionally, the US healthy snacks category is valued at $21.5B (Grandview Research). Despite the large opportunity at the intersection of these categories, dessert brands represented less than 9.5% of the Latinx-inspired food brands surveyed.

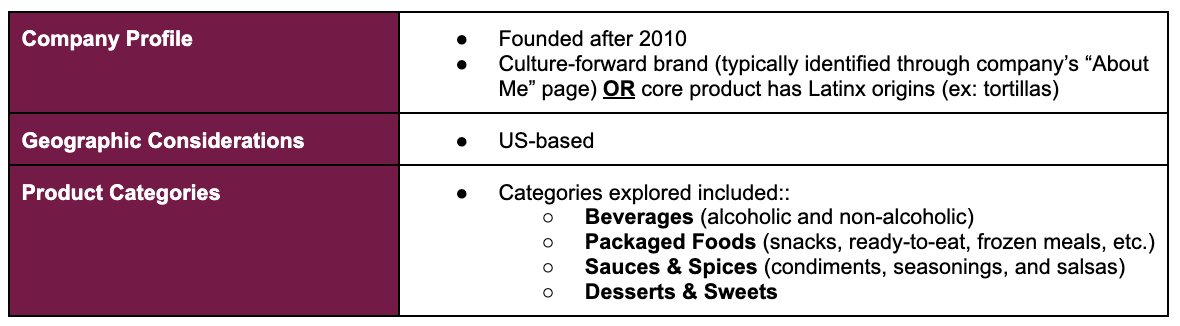

Criteria

The table below shows the criteria we used for selecting the data set, which includes the 63 companies that were reviewed for this analysis.

The History

The emergence of major Latinx food brands began to take shape in the early 1900s. While it is difficult to pinpoint the first company to appear on the scene, Goya Foods is often credited as one of the latest and greatest food companies that has significantly impacted Latinx culture. Founded in 1936 by Spanish immigrants Prudencio and Carolina Unanue in Manhattan, New York, the company started as a small business importing Spanish olives and has since grown to become one of the largest suppliers of Latin American food products, catering to a wide range of Hispanic and Latino communities across the country. Since then, other legacy brands have also grown to dominate the space, including Mission Foods (1949), Herdez (1914), La Preferida (1949), and La Costeña (1923).

Thanks to the aforementioned players' contribution, Latin American food is the third most popular cuisine in the United States, only behind American and Italian food. The growing Hispanic population in the US, which is expected to reach 22% by 2028, is also influencing the broader US palate. In 2020, the Latin American food market was valued at $25.8 billion and is expected to grow to $37.0 billion by 2028, representing a CAGR of 4.6%.

While legacy brands have historically dominated, many startup companies have come forth as they try to address the growing market demand, which has led us to the 63 companies in our study, shown below:

Trends

After analyzing the data from 63 companies, we found the following themes.

Beverage as the Dominant Category

Nearly 40% of the dataset is concentrated in beverage companies, which prompted a deeper investigation into the underlying factors driving this notable preference.

Across all cultures, many immigrants and their descendants crave traditional products and flavors that remind them of home. Beverages such as aguas frescas, horchata, and Mexican sodas are cultural staples within Latinx communities. As a result, entrepreneurs have tapped into this nostalgia, creating companies such as Agua Bonita (a Supply Change Capital portfolio company) and Mayawell that offer a modern take on these beloved drinks.

Furthermore, in understanding the difference between launching a food enterprise versus a beverage enterprise, it is clear that the beverage category seems to have more favorable dynamics:

Lower Startup Costs: Beverage companies often require less complex equipment and ingredients than food production

Longer Shelf Life: Many beverages, especially those that are pasteurized or contain preservatives, tend to have longer shelf lives than food products

Easier Scalability: There are many co-packers available for beverage companies, making it easier to scale without significant financial investment

Regulatory Environment: Beverage businesses, especially non-alcoholic, typically face fewer stringent health regulations compared to food businesses that may deal with perishable items such as meat or dairy

Mexico as the Dominant Heritage

We also observed that Mexico-inspired brands had the largest representation at 43%, followed by South America (27%), non-specific (21%), Central America (9.3%), Caribbean (6.4%), and Other (5.8%).

Given Mexican-Americans constitute nearly 62% of the U.S. Latinx population, Mexico's significant representation within our study aligns with expectations. In fact, Mexico has had and continues to have the greatest influence on the American palate across all Latinx cultures. According to a Datassential survey, 45% of Gen Z consumers would choose Mexican if they could eat only one cuisine for the rest of their lives. Additionally, an L.E.K. study revealed that Google searches for “Mexican food” saw an annual uptick of 27% from 2014 to 2019 and 18% from 2019 to 2021 (see figure below).

Prominent U.S. food brands have strategically positioned themselves to take advantage of this trend. For example, in 2020, Mexico-inspired Cholula Hot Sauce was sold to McCormick for 25x EBITDA due to the growth in demand.

West Coast as the Dominant HQ Region

Of all regions within the United States, the largest number of Latinx-inspired food brands are headquartered on the West Coast, with California having the highest concentration at 21 companies total. After California came Texas (10 companies) and Florida (8 companies).

Interestingly enough, a 2014 Annual Survey of Entrepreneurs by the United States Census Bureau showed that among the nation’s nearly 300,000 Hispanic-owned firms at the time, more than half were located in one of three states: California (66,487), Florida (59,987) or Texas (49,722).

More recently, Pew Research Center provided additional context for this phenomenon by reporting that of the 62 million Latinos living in the US in 2020, California, Texas, and Florida held about half of the U.S. Latino population.

The Investment Landscape

In terms of funding trends, some interesting statistics emerged:

To date, Latinx-inspired brands have raised approximately $200M in capital1

Of the ~$200M in capital raised for Latinx-inspired food brands, teams with at least one female founder have received more than 62% of all funds

Across all heritages, Mexico-inspired brands have raised the most capital at $122M

The average Mexico-inspired brand has received 1.25x more funding than South American-inspired brands and 1.30x more funding than Central American-inspired brands

67% of Mexico-inspired companies received funding within the first 5 years versus only 43% of South-American-inspired companies

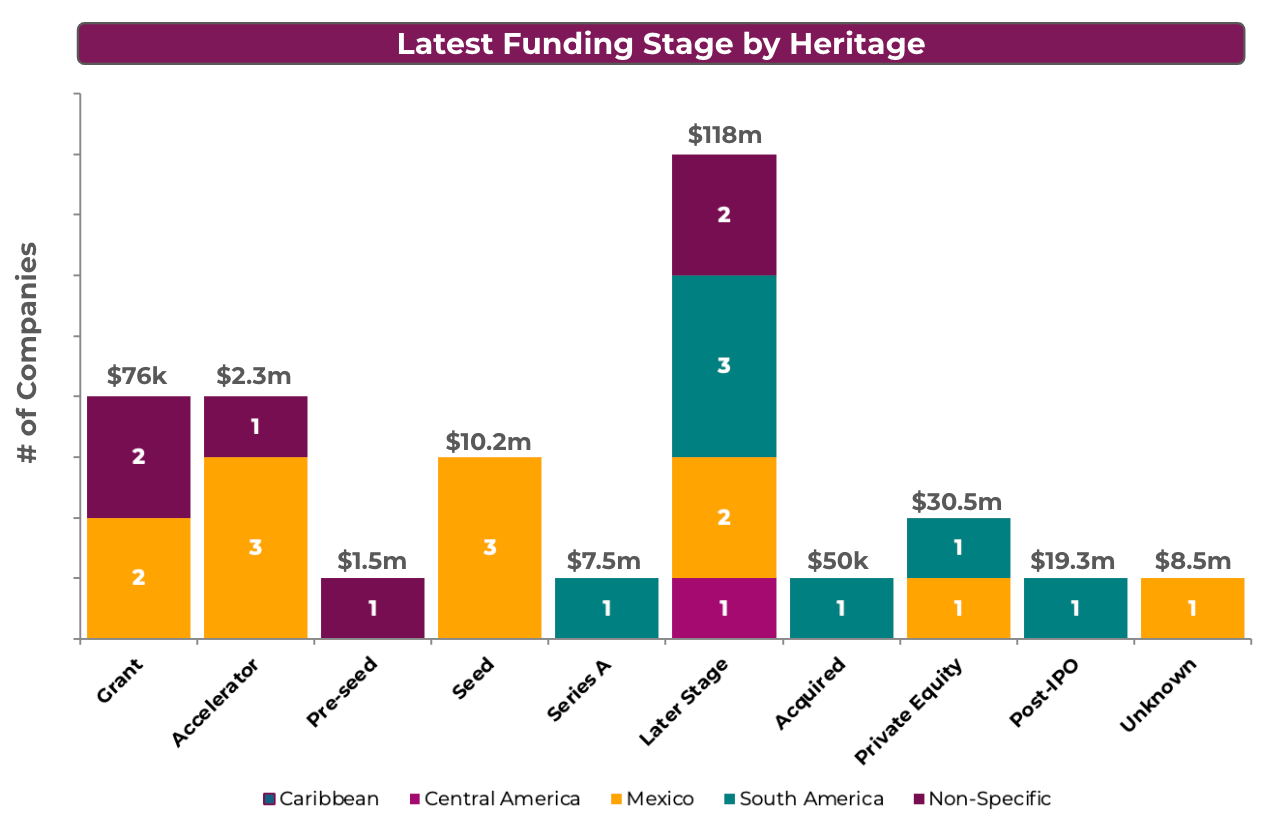

We were also interested in analyzing the amount of capital raised at each funding stage while comparing it to the number of heritage-inspired brands at each stage, as shown below. This graph indicates the pent-up momentum for many of these Latinx-inspired brands that currently exist at the “later stage” of funding and are likely ripe for a near-term exit.

Trends Amongst Genders

Despite women representing over half of the United States population, Carta reported that in 2023, women accounted for only 13.2% of startup founders across the country. Our study revealed that Latinx-inspired brands are much more in line with the nation’s population distribution. Across all 63 companies, 51% of the founding teams had at least one female founder, and 43% of the companies had women as CEOs.

The Investors

After examining trends across companies, we felt it was imperative to also understand the investors who are backing these brands. As such, we identified nearly 100 unique investors, including 29 VC firms, 23 angel investors/angel groups, 9 corporate investors / VCs, and 9 accelerators/incubators. VCs represented the largest segmentation at 33%, with Growth / Expansion firms having the smallest representation at 5%.

Collectively, all of the investors have +$12bn AUM2 and have made an average of 100 investments across their portfolios and industries. In terms of geography, and similarly to the breakdown of our company’s headquarters, the West has the largest representation by firm count and AUM3.

Exit Landscape

While many of these Latinx-inspired brands are still in their infancy, there have been four successful exits for companies founded 2010 or later that are worth noting.

Heritage-inspired Mexican-American foods for a variety of dietary needs and preferences, Siete Foods, announced a $1.2B 2024 acquisition by PepsiCo (Recently, Stripes Group invested $90m in Siete Foods in exchange for a minority stake)

Gluten-free, Brazilian-style cheese bread company Brazi Bites was acquired by San Francisco Equity Partners in 2018 for an undisclosed amount

Chosen Foods, a sustainably sourced, high-quality avocado products company, was acquired by Butterfly Equity in September 2021 for an undisclosed amount

As shown below, we have seen a slight uptick in legacy brand acquisitions for strategic corporate acquirers over the last 10 years for legacy brands. Considering the companies within our study, this activity bodes well for their future exit potential.

The Opportunities

The Hispanic/Latinx population in the US is one of the most influential consumer segments, with a total economic output of $3.2 trillion in 2023, according to a report by the Latino Donor Collaborative. Furthermore, it was reported that the purchasing power of the Latinx population in America is estimated at $3.4 trillion, and if they were a standalone economy, they would have the fifth-largest GDP in the world. This growth is creating opportunities for entrepreneurs and investors alike within the food and beverage category. As such, we have outlined a few thoughts on the opportunities within the space.

Caribbean and Central-America-Inspired Foods

As of 2020, the US Caribbean (Puerto Rico, Cuba, Dominican Republic & Haiti) and US Central American (El Salvador, Guatemala, Honduras & others) population collectively accounted for 25.7% of the entire US Latinx population (US Census). With less than 10% of Latinx-inspired brands representing these two cultures in our analysis, the marketplace has a clear opportunity to align food brand options more closely to the larger US Latinx population. While we have identified brands such as Bayjoo and A Dozen Cousins that appeal to the Caribbean heritage, this white space is the prime landscape for entrepreneurs looking to penetrate the space.

More Latinx-Inspired Dessert Options

Consumers’ increased concern for their health and well-being has increased demand for “better-for-you” dessert options. Therefore, investors and entrepreneurs should be increasingly focusing on brands that cater to niche markets within the dessert segment, such as plant-based, low-sugar, and keto-friendly options. Recent M&A activity within the space supports this recommendation (see figure below).

Ecosystem Support

Participating in Latinx-Focused Accelerators

According to a study conducted by the Harvard Business Review, startups participating in an accelerator raised 50% to 170% more from investors and were more likely to be acquired than similar startups that applied to the accelerators but were not accepted. Therefore, Latinx founders who are serious about growing their business should highly consider participating in an accelerator program at some point in their journey.

We have identified a few Latinx-focused startups, including:

Google for Startups Latino Founders Fund: provides $150,000 in non-dilutive capital and hands-on support to help Latino entrepreneurs build and grow their businesses in the US

Accelerate Latinx: A seven-month bilingual accelerator program in Houston that helps small businesses grow

The Brazi Bites Latino Entrepreneur Accelerator Program (LEAP): a program designed to help small Latino-owned business owners; the winner receives a $10K business grant, a 12-week mentorship from the Brazi Bites team, free legal advice, and more

AWS Impact Accelerator for Latino Founders: An eight-week program that helps Latino-led startups scale their cloud-based businesses; startups receive a $125,000 unrestricted cash grant and $100,000 in AWS Activate credits

Summary

The Latino GDP in the U.S. has surged to $3.2 trillion, reflecting significant economic influence. The 2023 Latino Business Action Network and Stanford report highlights rapid growth in Latinx entrepreneurship, with a 44% increase in new businesses over the past decade. However, many sectors remain controlled by long-standing incumbents, underscoring opportunities for investments tailored to the Latinx community. As M&A activity rises, particularly in sectors with untapped potential, there’s a growing demand for by-and-for community investments that can harness this economic momentum.

Help us build on our work:

You can find a full list of companies we analyzed in this Airtable database here

Are you building a Latinx-inspired brand that you would like to share with us? Fill out our intake form here

Who did we miss? Share details in this survey here

Data pulled as of July 2024 and only accounts for 25 companies where we were able to identify capital raised via Pitchbook

Angel Investors / Groups were not included

Angel Investors / Groups were not included

Thanks for sharing, Alyssa! I really appreciated learning about the overlooked opportunities in Latinx-inspired food categories, which present a strong case for culturally rooted innovation driving growth in the venture world

Love how you're shedding light on the immense cultural influence behind Latinx-inspired food brands and highlighting the opportunities for growth in underrepresented regions and product categories—exciting insights!